A liability shift is the moment under card-scheme rules when responsibility for a fraudulent transaction moves from one party to another. The most common example is the 3D Secure authentication liability shift: a successful 3DS2 authentication moves chargeback liability for fraud-related disputes from the merchant to the issuer. EMV chip-and-PIN at the point of sale moves card-present liability in a similar way.

Travel payments glossary

Liability shift

When responsibility for a fraudulent transaction moves from one party to another under scheme rules.

Why it matters in travel

For travel, liability shifts are one of the few levers that meaningfully reduce chargeback exposure on high-value card-not-present bookings. A robust authentication flow is the difference between defending fraud chargebacks at high cost and not having to defend them at all.

The economics of a single fraud chargeback on a £6,000 booking are unforgiving. Even if representment succeeds, the operational hours spent gathering evidence — supplier confirmation, communication trail, authentication logs, delivery proof — usually outweigh the recovered amount. Multiply that by an exposed quarter and a single hole in the authentication setup becomes a real line in the P&L.

The teams that lean into liability shift treat authentication as a product question, not a compliance one. They invest in flows where the customer experiences a single biometric prompt inside their banking app and is back to checkout in seconds, rather than the older redirect dance that broke conversion. The shift in chargeback liability comes as a side effect of building the better customer experience.

How felloh helps

felloh records the authentication evidence that drives a liability shift alongside the booking, so when a chargeback does land the shift can be invoked with the evidence already in place.

The Transactions view in the dashboard records the 3DS outcome, exemption claim and liability-shift status against the booking, so the evidence is preserved before any dispute arrives. The Chargebacks workflow surfaces representment cases where the shift applies, so the response either invokes the shift or moves to the next evidence pack as appropriate.

For travel businesses defending high-value CNP disputes, the shift becomes a routine outcome rather than a case-by-case argument. Chargeback win rates rise, representment effort drops, and authentication policy gets tuned against measured outcomes.

Where this shows up in risk and disputes.

Liability shift touches more than one workflow at felloh. Start with the pages most travel teams reach for next.

- Financial Control

Control refunds, exceptions, supplier exposure and payment risk against the same booking record.

Explore - Financial Protection Data

Authentication, settlement, protected funds and refund history kept with the booking for dispute defence.

Explore - Payment Optimisation

Acceptance, decline and authentication evidence so you can act on the patterns that matter.

Explore

More on payment risk and disputes.

Real-world context from the felloh team and customers, written for travel finance and operations.

Updates

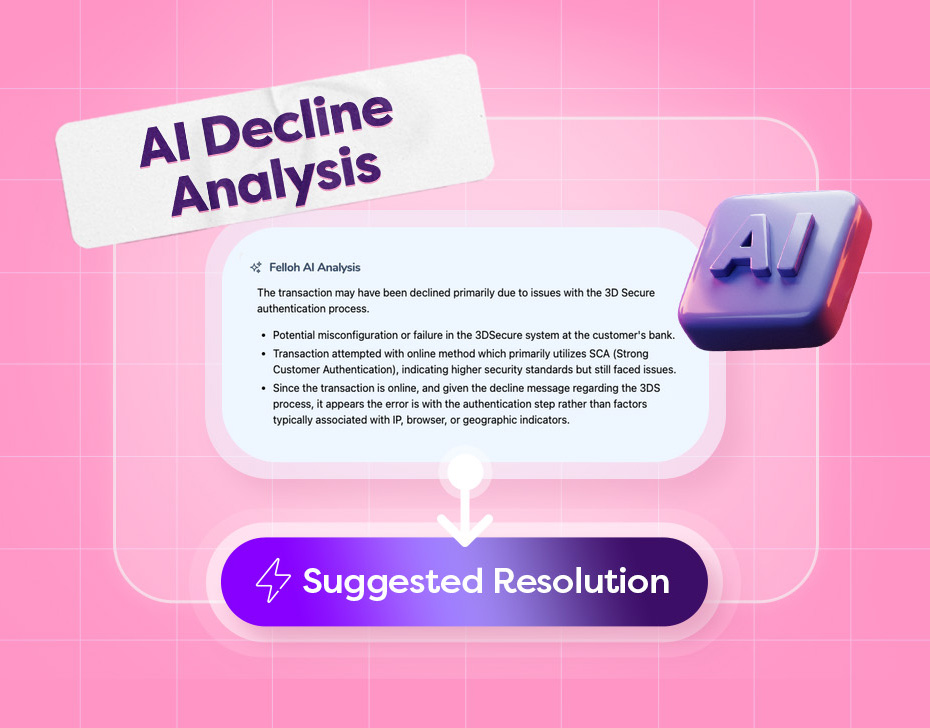

UpdatesEnhance Your Payment Success with felloh's AI Decline Analysis for the Travel Industry

felloh's AI Decline Analysis surfaces real-time insight on why card payments fail and the best next step — for higher acceptance on travel bookings.

Read article Insights

InsightsMinimising Payment Risks of phone payments: The Smart Way for Travel Merchants

Phone bookings are still essential in travel, but they carry payment-security risk. How to keep last-minute trips moving without exposing the business.

Read article

Connect the dots.

See how payments, settlement, refunds and reporting evidence connect around every booking.