The latest news, thoughts and insights from our experts in travel payments

Updates

Giving AI agents access to travel payments: introducing the felloh MCP server

We’ve launched the felloh MCP server to make our connected travel payment infrastructure directly accessible to AI agents through natural language. Rather than manually navigating dashboards or writing custom API "glue," you can now use tools like ChatGPT or Claude to orchestrate complex workflows all while staying grounded in your existing operational controls. This isn’t a separate product, but a new conversational layer that complements our APIs and SDKs, allowing your team to interact with your operational stack in the way that fits you best.

We love sharing our travel expertise, so we're always creating new resources to help travel businesses succeed.

Free guide

Everything travel businesses need to know about chargebacks

Running a travel business is challenging enough without having to deal with chargebacks eating into your profits and taking up valuable time. This FREE practical guide covers 5 proven strategies on how to avoid them.

Everything travel businesses need to know about chargebacks

Running a travel business is challenging enough without having to deal with chargebacks eating into your profits and taking up valuable time. This FREE practical guide covers 5 proven strategies on how to avoid them.

Everything travel businesses need to know about chargebacks

Running a travel business is challenging enough without having to deal with chargebacks eating into your profits and taking up valuable time. This FREE practical guide covers 5 proven strategies on how to avoid them.

We love sharing our travel expertise, so we're always creating new resources to help travel businesses succeed.

Free guide

Everything travel businesses need to know about chargebacks

Running a travel business is challenging enough without having to deal with chargebacks eating into your profits and taking up valuable time. This FREE practical guide covers 5 proven strategies on how to avoid them.

Free guide

Everything travel businesses need to know about chargebacks

Running a travel business is challenging enough without having to deal with chargebacks eating into your profits and taking up valuable time. This FREE practical guide covers 5 proven strategies on how to avoid them.

Free guide

Everything travel businesses need to know about chargebacks

Running a travel business is challenging enough without having to deal with chargebacks eating into your profits and taking up valuable time. This FREE practical guide covers 5 proven strategies on how to avoid them.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Insights

Will Bicknell

Payments is full of jargon and several different parties to make it happen, here we explain how it all fits together and the Role of Merchant Acquirers, Card Schemes and Card Issuers in the UK

Who's who in card payments

What to do next?

1

Automate your manual tasks with AI-powered Software as a Service

You don’t need in-house AI tools to do this, most software providers will be doing the heavy lifting for you

2

Step up your SEO and AI Optimisation (AIO) strategy

Make sure your experiences are easily discoverable in consumer-generated itineraries. If you’ve invested in search engine optimisation (SEO) in the past, a lot of that work will be paying off now, but if not, it’s never too late to tag your images, set meta descriptions and make sure your most important content is machine readable.

3

Experiment cautiously with customer facing AI tools

If you’re not yet using any AI in your business, now is not the time to rip out your search function on your website and replace it with an AI chat bot! As an end consumer you probably know how frustrating it can be to deal with a poorly trained bot. Instead, find a problem you have which is worth solving but not business critical to start learning in a low-risk environment.

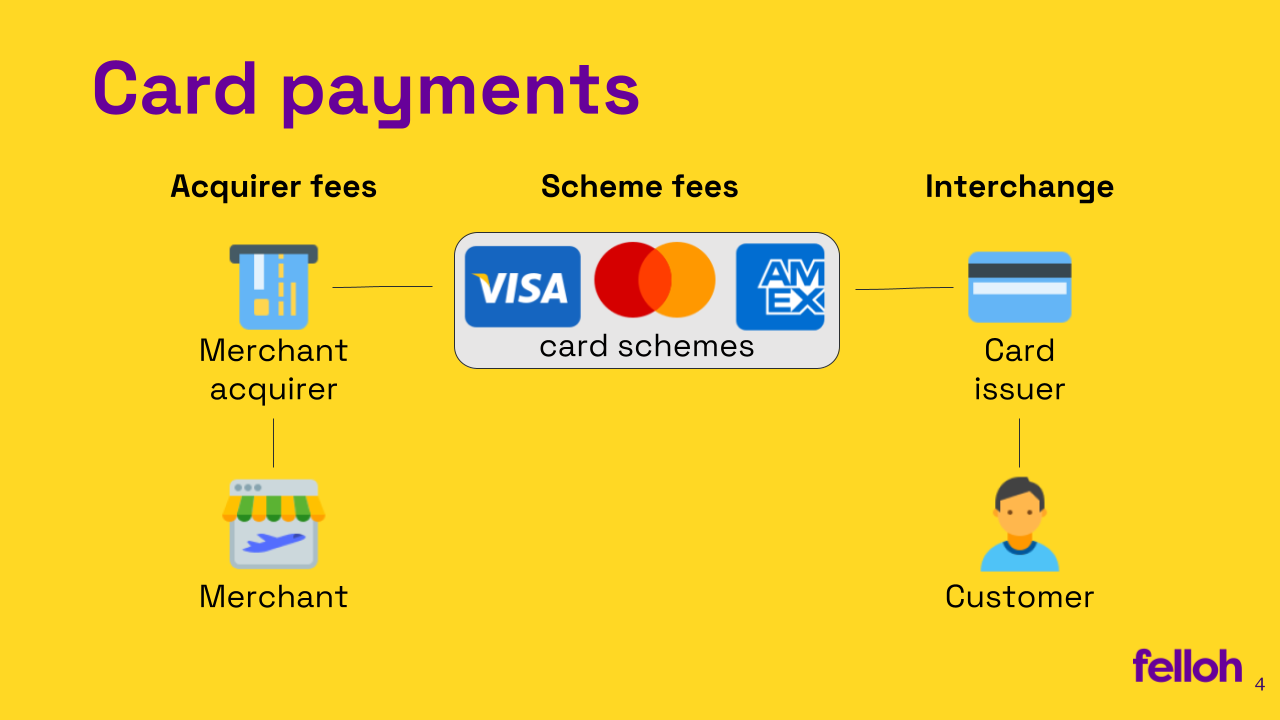

When you make a payment with a credit or debit card, there are a number of different organisations involved in processing the transaction. These include the merchant acquirer, the card scheme, and the card issuer.

The merchant acquirer is the financial institution that works with merchants, in our case travel agents or tour operators, to accept credit and debit cards. The acquire collect the payments from the cardholder's bank and then send the funds to the merchant.

Thecard scheme is an organisation that sets the rules for how credit and debit cards are used. Card Schemes also provide the infrastructure that allows merchants and cardholders to connect with each other. The most well-known card schemes in the UK are Visa, Mastercard, and American Express.

The card issuer is the bank or financial institution that issued the credit or debit card to the cardholder. The issuer is responsible for managing the cardholder's account, including processing payments, setting spending limits, and issuing refunds.

When a cardholder makes a payment with a credit or debit card, the following steps take place (I have skipped some authorisation and fraud checks for simplicity)

The merchant swipes the card or enters the card details into a payment terminal or the cardholder enters their own details in a form.

The merchant acquirer and the card issuer each charge a fee for processing card payments. These fees are known as scheme fees and interchange.

Scheme fees are charged by the card scheme to the merchant acquirer. These fees cover the costs of operating the card scheme, such as fraud prevention and marketing.

Interchange is charged by the merchant acquirer to the card issuer. This fee covers the costs of processing the payment, such as authorisation and settlement.

The amount of scheme fees and interchange charged for a card payment varies depending on the type of card, the amount of the transaction, and the merchant's location.

.png)

.png)

.svg)

.png)

.png)

.svg)

.svg)

.avif)

.png)

.png)

.png)

.svg)