Heading to WTM London? Come find us at stand S3-116. We’ve more than good coffee brewing. ☕ Pre-book a chat now!

Felloh automatically detects corporate and international cards at checkout and applies the appropriate surcharge in real-time. Your customers see exactly what they'll pay, with the option to switch payment methods if they wish to avoid the surcharge. No more manually checking card types or calculating fees – it's all handled instantly and compliantly.

Recover processing costs on eligible cards without absorbing fees or manually calculating surcharges

Our system only applies surcharges to eligible cards (corporate and international), fully compliant with Payment Surcharge Regulations

Customers see fees upfront with the option to use a different card or payment method

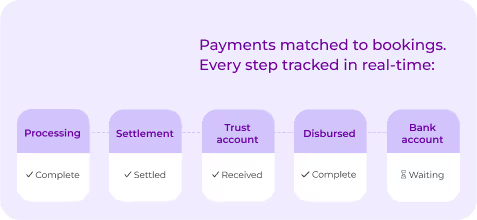

No more manual matching of mysterious bulk settlements to individual bookings

Track the entire payment journey from initiation to settlement in your bank account in real-time

Automatic matching means no more spreadsheet mistakes or misallocated payments

"To be compliant when you apply a surcharge, you must only charge the exact amount you pay for international or corporate card payments. Felloh's technology detects the card type and applies precisely the right surcharge – keeping you compliant while recovering your costs."

Chris Jones

COO