For many travel companies, card surcharges feel like a thing of the past. Before 2018, it was common practice to pass on 1–2% card processing fees to customers. Then new legislation came in, and almost overnight, the industry stopped adding surcharges altogether.

The knee-jerk reaction was simple: “We’re not allowed to surcharge anymore.”

But that’s not the whole story. In fact, while the UK and EU legislation banned surcharges on consumer debit and credit cards, it left the door wide open for businesses to legally apply surcharges to corporate and international cards. Understanding this distinction is important, because ignoring it often means travel merchants end up absorbing unnecessary processing costs.

What the law really says (the Myth-Busting facts)

The legality of surcharging is not universal; it varies significantly by region. While many in the travel industry reacted to the 2018 EU and UK ban, the rules are very different in other major markets.

- UK and EU: The Payment Services Directive 2 (PSD2) banned surcharges on consumer debit and credit cards. However, the ban does not apply to corporate or international cards.

- Australia: Surcharging is permitted in Australia, but it is heavily regulated to ensure the surcharge does not exceed the actual cost of accepting that card type. There is also a ban on excessive surcharges on most credit, debit, and prepaid cards.

- Canada: Following a legal settlement in 2022, Canadian merchants can apply a surcharge to credit card transactions. However, surcharges are not permitted on debit or prepaid cards. The surcharge amount is capped at 2.4% and cannot exceed the merchant's discount rate.

- United States: Surcharging is generally legal in most states, but the laws are complex and vary. While many states permit surcharging, some, like Connecticut and Massachusetts, have restrictions or outright bans. Federal law caps surcharges at 4%, but many card networks, like Visa, limit them to 3%. Merchants must disclose the surcharge at the point of entry and the point of sale.

The core principle across these regions is similar: if surcharging is permitted, you can only pass on your actual costs, not add an extra fee for profit. For example, a US-issued American Express card might cost you 1.95% in processing fees, while a US-issued Visa card might cost 2.50%. If you charged all US cardholders 2.5%, you would be overcharging your Amex customers, which is not compliant.

How travel businesses can stay compliant (without headaches)

The challenge is knowing which cards qualify for surcharges - and at what rate - in real time. That’s where technology comes in.

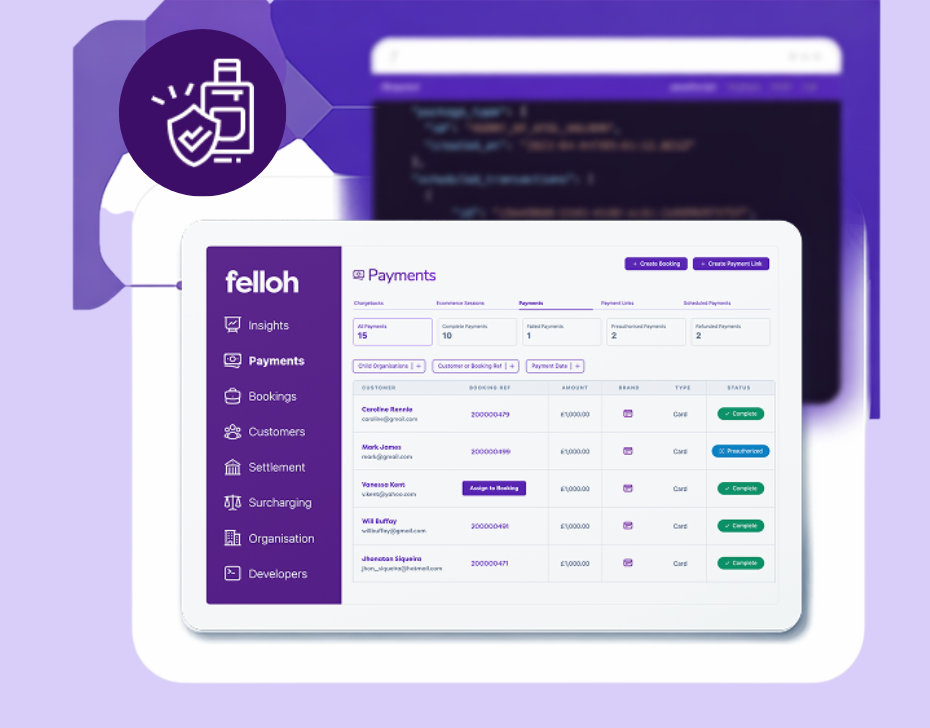

At Felloh, our automatic surcharging feature does the heavy lifting:

- Card identification at checkout

Every card has a unique BIN (the first six digits on the card). By running a BIN lookup, we can instantly detect whether it’s a consumer, corporate, or international card.

- Exact fee matching

Because Felloh is deeply integrated with acquiring banks, we don’t just stop at “corporate” or “international.” We can see the exact processing cost associated with that card type.

- Precise surcharge calculation

We automatically apply the correct surcharge - no more, no less - ensuring you’re fully compliant while recovering your costs.

So far this year, Felloh has helped travel businesses recoup more than £78,000 in card processing costs. One customer with a large international client base, The Small Cruise Ships Collective, have recovered 46% of their processing costs thanks to automatic surcharging.

Why this matters for your travel business

For travel companies operating on tight margins, processing fees on international and corporate cards can add up fast. By using compliant, smart surcharging, you can:

- Protect margins without falling foul of legislation.

- Ensure fairness for customers—each cardholder only pays what their transaction really costs.

- Automate the process, so there’s no manual calculation or risk of error.

- Save time, allowing your team to focus on providing exceptional travel experiences.

Key Takeaway

Despite the industry myth, surcharging is not dead. The 2018 ban in the UK and EU only applies to consumer cards - not corporate or international ones. Furthermore, many other global markets have their own surcharging regulations, which travel businesses can use to their advantage.

With Felloh’s automatic surcharging, you don’t need to second-guess the rules or build manual workarounds. We identify the card, match the cost, and apply the surcharge - seamlessly and compliantly.

👉 If you’ve been absorbing unnecessary processing fees, now’s the time to explore how Felloh can help.

.svg)

.png)

.png)

.png)

.png)

.svg)

.avif)

.png)

.png)

.png)

.png)

.png)

.png)

.svg)